Audio By Carbonatix

[

{

"name": "GPT - Leaderboard - Inline - Content",

"component": "35519556",

"insertPoint": "5th",

"startingPoint": "3",

"requiredCountToDisplay": "3",

"maxInsertions": 100,

"adList": [

{

"adPreset": "LeaderboardInline"

}

]

}

]

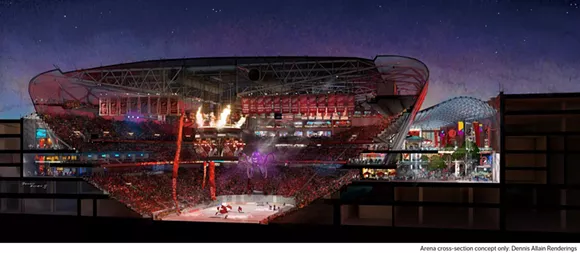

Via Olympia Development of Michigan

New Detroit Red Wings arena cross-section rendering.

The Detroit Downtown Development Authority (DDA) today approved the convoluted sale of $450 million in bonds to finance the construction of new Detroit Red Wings arena near downtown.

The financing plan calls for a revised structure unlike the preliminary proposal approved last year; for instance, the cap on state school taxes that can be captured by the DDA to pay off bonds has been lifted, and the DDA may enter into a financial gamble known as an interest rate swap to hedge floating interest rate payments.

The Michigan Strategic Fund (MSF), the state entity that will issue bonds for the project, is expected to consider the agreement at a 2 p.m. meeting tomorrow in Lansing.

The vote comes just weeks before Red Wings owner, Ilitch Holdings Inc., is expected to break ground on the eight-story arena, which will seat approximately 20,000 people and be owned by the DDA. The Red Wings current home, Joe Louis Arena, is expected to be demolished using $6 million in state funds within six months after the team moves to the new facility.

According to plans released by Olympia Development of Michigan (ODM), the real estate arm of Ilitch Holdings, the new 785,000-square-foot arena will be situated in an area bounded by Woodward Avenue, Henry Street, Sproat Street, and Clifford Street. A groundbreaking is slated later this month, with the majority of construction work expected to begin next spring. Project backers say the arena will open in time for the National Hockey League's 2017-2018 season.

Understanding the structure of the deal to finance the arena takes a bit of work — a point acknowledged by a number of officials and project backers during the meeting today. (It's complex!)

In layman's terms, what's going on here is a daisy chain of borrowing: The DDA will sell $450 million in bonds to the MSF. In turn, the MSF will sell those bonds to finance the construction of the arena. The MSF bonds will be paid off by three revenue streams: $15 million or more in state school taxes the DDA can legally capture, $2 million in a separate DDA tax capture, and ODM's annual $11.5 million fee.

(Simply put: Because the bonds will be secured by DDA revenue, the DDA initially has to sell bonds to the MSF. In actuality, the financing scheme entails a $450 million bond sale in total that's secured by those three revenue streams. Confusing, we know.)

Public funds will account for 53 percent of the arena cost, at $285 million; ODM will account for the remaining 47 percent, at $250 million, which includes funds the company has spent acquiring land on the arena site.

The specifics, according to a Sept. 10 report to the DDA's board of directors, are as follows:

- Through an agreement arranged with the MSF, the DDA will sell $450 million in bonds to the MSF that will be separated into two groups: $250 million in 30-year tax exempt bonds, and $200 million in 30-year taxable bonds.

"It is necessary to separate the financing into two series of bonds because [the bonds secured by public money] are federally tax exempt because they will be repaid from the pledged tax-increment revenues," the report says.

Under state law, the DDA can capture the increased property tax revenue generated as a result of new development, called tax-increment financing, or TIF. (We covered TIF in this week's cover story on the Detroit Economic Growth Corporation (DEGC), the private entity that negotiated the arena deal on behalf of the City of Detroit.) It's expected that annual DDA TIF revenue will increase as a result of the new arena.

- In turn, the MSF will issue $250 million in tax-exempt bonds that will be purchased by Bank of America, according to DDA Treasurer John Naglick. Bank of America will then offer those bonds in denominations of at least $250,000 to the public. These bonds will be repaid by roughly $15 million in state school taxes the DDA is legally allowed to capture for the project, and a separate $2 million annual DDA tax capture (read: public money).

Previously, the memorandum of understanding passed last year between ODM, MSF, and the DDA called for a $15 million annual cap on the use of state school taxes to repay the bonds. But, in a surprising development, under the preliminary agreement approved today, that cap has been removed.

"Based on requirements of [Bank of America], this cap has been removed to in order to increase the amount of [public revenue] projected to be available to repay the [bonds secured by public money] and thereby strengthen the creditworthiness of [those bonds] so that a 'BB' rating can be obtained," the report says.

The preliminary agreement from Bank of America to purchase the entire $250 million in bonds is subject to a rating from Fitch of no less than "BB," the report says. To date, the report says Fitch has "not completed its review and no rating has been issued" to the bonds secured by public money.

A number of financial backstops are built into the proposal in the event the TIF revenue doesn't materialize, according to the report.

- The MSF will also issue $200 million in floating rate bonds that will be purchased by Comerica, according to Naglick. These bonds will repaid by the $11.5 million annual fee paid by ODM. As Naglick explains, these bonds will be privately kept on Comerica's books and not sold to the public.

According to a loan agreement approved today, this series of limited obligation bonds can be repaid "solely" from ODM revenues generated at the arena, "without recourse to any tax increment revenues or any other revenues of the [DDA] ... or to any other properties or assets, now owned or hereafter acuired, tangible or intangible, of the [DDA]"

- As Metro Times first reported last week, the DDA anticipates it will enter into an interest rate swap on the $200 million bond issue secured by ODM revenue. This would take place as part of the agreements approved today.

The swap, essentially a financial gamble, allows the DDA to synthetically fix the interest rate, and assumes a benchmark interest rate used by financial institutions across the world will rise, rather than fall.

The swap would last until the bonds are retired life in 2045. In return for the fixed rate the DDA will pay a yet-to-be-named counter-party (that will be later identified by ODM), the DDA will receive a variable interest rate payment from the counter-party based on LIBOR, the London Interbank Offered Rate, an interest-rate benchmark. Last month, the DDA sought a swaps adviser on the deal, and, according to documents, selected New York City-bsed firm Mohanty Garglulo.

Heber Farnsworth, associate professor of finance at Penn State University's Smeal College of Business, told Metro Times in our cover story last week, if the DDA actually pursues the swap, the authority would come to an agreement with the counter-party as to what both sides believe the LIBOR rate will be when the swap kicks in — likely in 2018.

If the DDA's gamble heads south, Farnsworth offered a possible worst-case scenario: For instance, if the LIBOR rate drops, the DDA could be stuck with paying a fixed rate, while receiving a smaller amount in return from the counter-party. If that happens, and the DDA is on the "losing" side of the bet, it might have to post collateral — similar to how Detroit posted its casino revenue when the city's infamous interest rate swaps went sour.

Detroit agreed to spend $85 million to terminate its swaps agreement with Bank of America and UBS; the Detroit Water & Sewerage Department had to spend a whopping $571 million on termination fees for a sour swap.

Interest rates are expected to rise in the coming years. But, as Farnsworth put it, over the next three decades, LIBOR is expected to rise and fall — again and again. If rates are pushed as low as they have been since the 2008 recession, then the DDA may be on the losing side of the swap.

If the DDA were to then miss a swap payment, the counterparty could simply "seize all the collateral," Farnsworth says. But whatever the DDA could possibly post as collateral is entirely unknown.

It's unclear what the terms of the swap may entail, but the report says an agreement will be presented to the DDA board prior to the $200 million floating rate bond sale.

A stipulation of the Concessionaire Management Agreement (CMA) reached last summer stated ODM must invest, or "cause to invest," $200 million in private adjacent development to the new Red Wings arena.

Brian Holdwick, Detroit Economic Growth Corporation executive vice president of business development, told the DDA board today the $200 million in private investment could include everything from planned housing and retail developments, to "tens of millions" of dollars in infrastructure upgrades ODM says it has committed to spend for landscaping improvements, street upgrades, and new streetlights.

What it can't include, according to Holdwick, is surface parking lots — a sea of which already surround nearby Ilitch-owned properties. If the $200 million in private investment is spent within five years of the first event at the new arena, then ODM will be reimbursed as much as $74 million in public money by the DDA, Holdwick says.

PLANNING BOARD ASKED TO REZONE SITE

Meanwhile, ODM outlined some aspects of the expected $200 million of private investment in site plans the Detroit City Planning Commission will consider this week. The commission is being asked to rezone the arena site to fit ODM's proposal.

The arena site will include a piazza that's half the size of Campus Martius, according to Richard Heapes, of Street-Works Development, one of the numerous firms involved in the project. The piazza could potentially be used for separate ticketed events, but will serve mainly as a greenspace outside the arena entrance.

The plans also call for a parking structure with 1,200 spaces will line Cass Avenue between Henry and Clifford streets. ODM proposes to build 184 housing units along the western and southern edges of the arena. This would include 56 efficiency lofts at 690 square feet, 20 efficiency studios at 475 square feet, 8-one bedroom units at 960 square feet, 64 one-bedroom units at 710 square feet, 20 two-bedroom units at 970 square feet, and 16 townhouses at 1,365 square feet.

The plans call for the City of Detroit to permanently vacate a number of streets, including: Park Avenue, between Henry and Sproat, as well as Sibley Street between Clifford and Woodward. ODM also asks for restrictions on what type of business can be authorized in the arena site; under the deal approved today, topless strip clubs, gun shops, and even tarot-card readers would be banned from the so-called catalyst development district.

The planning commission meeting will take place Thursday, Sept. 18 at 5 p.m. inside the Erma Henderson Auditorium on the 13th floor of the Coleman A. Young Municipal Center, which is located in downtown Detroit at 2 Woodward Ave.